Full Checklist

Every milestone across all 9 chapters. Track your raise from first list to final wire.

Why This Exists

Most fundraising advice is either too high-level to be useful or too anecdotal to be repeatable. Founders piece together guidance from blog posts, Twitter threads, and war stories from founders who raised in different markets, at different stages, with different networks. The result is a process built on incomplete information, borrowed instincts, and a lot of avoidable mistakes.

This playbook gives you a repeatable, data-driven process — one that works whether you're raising a pre-seed round with no revenue or a Series A with $2M ARR. The specifics will change. The process won't.

Who This Is For

Founders raising pre-seed, seed, or Series A rounds. Where the specifics differ — traction bars, check sizes, investor types, what investors are evaluating — we call it out directly.

If you're raising a growth round or beyond, some of this will still be useful — but the dynamics are different enough that this guide isn't optimized for you.

How to Read It

Nine chapters in order — from investor list to wiring the money. Each chapter ends with a milestone gate that tells you when you're ready to move on. Read through for context, but don't skip steps when running the playbook, except for chapters 3, 4, and 5, whose activities will likely run in parallel. The most common reason rounds stall is jumping to step seven before steps one through six are done.

A Note on the Venture Ecosystem

Fundraising is not a meritocracy. Access, networks, and relationships matter enormously — and that's not changing. What this playbook does is give you a systematic way to build the access and relationships you need, regardless of where you're starting from. It won't eliminate the advantages that come with an established network, but it will close the gap faster than anything else available to you.

Build Your Target Investor List

The goal is a qualified list — not just a big one. Applying hard and soft filters to your initial universe leaves you with 70–120 investors who convert at 3–5× the rate of an unfiltered list. Time is the scarcest resource in a fundraise — make every conversation count.

Countless founders make the same costly mistake: blasting emails to thousands of investors. More meetings do not equal more checks. Investors routinely take meetings with non-fit founders to hit internal deal flow quotas and show activity to their LPs. Stage-mismatched meetings exist for investor benchmarking — not for you.

→ noise

This is the start of you building your investor list. Now is the time to create a spreadsheet and start tracking your pipeline.

Start building your list ↗Building your list is Phase 1 of 3 in your fundraise. Don't move to Phase 2 until Phase 1 is done.

Before building your list, know what type of investor you're targeting — each plays a different role in a round. The most important distinction: who can lead, and who can only follow.

Additional nuance: repeat founders (especially in AI) often command higher valuations and different terms. If the data says you're not ready — go back and build.

Start your search with the basics — these will help narrow your search dramatically.

These are non-negotiable filters. Fail any one of these, and the investor comes off the list.

in your sector

Small funds: at least 3 deals in your space

Remove from list

at your stage

More is better

No exceptions

in your market

Or meaningful regional presence

Hard no

in their portfolio

Adjacent is fine; direct is not

Off the list immediately

in last 6 months

Active = they have capital to deploy

Likely out of capital

These don't eliminate investors — they determine how much of your time they deserve. Tier your list: T1 (pass all) gets 70% of your time, T2 (fail 1) gets 25%, T3 (fail 2+) gets 5%.

Map Your Network

You have 70–120 qualified investors in your CRM. This chapter has one job: for every investor on that list, identify at least one person who can introduce you. Research and audit only — no outreach yet. Output: connector column filled in for every investor.

A connector is someone with a real, warm relationship with the investor — not just a mutual LinkedIn connection. Tier determines impact not just on getting a meeting, but on getting a check.

Tier 0 is your most powerful lever but most early founders won't have it. Tier 2 is your most realistic path.

Don't know any portfolio founders yet? Here's how to build those relationships from scratch:

- Founder communities and alumni networks — Slack groups, accelerator alumni circles. Shared identity builds trust and makes introductions more natural.

- Engage as a customer — If you genuinely need their product, a demo or sales call is a natural entry point for a real connection.

- Industry events and conferences — Research who's attending before you go, come with specific questions, always follow up afterward.

- Cold email to founders, not investors — Works if it's personal and offers something of value. Cold email to investors almost never works. Cold email to founders sometimes does.

- Content collaboration — Podcasts, panels, or joint articles build relationships while establishing thought leadership simultaneously.

For each investor, run this audit sequence:

Not everyone at a VC firm can write a check. Your connector must introduce you to a partner — not anyone below. Here's how firm hierarchy works:

When running the audit in 2.3, always identify the specific partner at each fund. Update your CRM accordingly.

- 75% of your investor list has a Tier 0–2 connector identified

- All connectors are tiered in CRM

- "No connector found" investors are flagged — not removed

- Realistic path to 60+ promised intros from Tier 0–2 only

Track two things per connector: who they are (name, tier, relationship context) and where they are in the process:

Add notes on any commitments made and how you know them. This feeds directly into Chapter 3 when you're collecting promises and Chapter 6 when you fire everything simultaneously. Don't rely on memory — by the time you have 40+ connectors in motion, the details blur fast.

Set up your pipeline tracker ↗Line Up Warm Intros

You have your list. You have your connector map. Now the work begins. Turn identified connectors into promised introductions — for every investor on your list. You are not pitching investors yet. You are collecting commitments.

Getting a meeting is not the end goal. Getting a check is. A strong intro doesn't just open a door — it transfers credibility. When a founder who an investor trusts vouches for you, that social proof follows you through every partner meeting, every reference check, and every moment of doubt in the process.

The intro also signals that you operate with discipline. Founders who show up organized, with a clear ask, via someone the investor trusts — those founders are easier to say yes to before the meeting even starts.

The double opt-in is the standard for warm intros. It protects the connector's relationship with the investor, respects the investor's time, and means every intro that reaches them arrives pre-qualified. Here's how it works:

The system only works if you have a sharp blurb (Chapter 4 covers this). Write it before you start making calls.

For your connector calls, be clear on what you're trying to walk away with: a confirmation from the connector that they know the investor well, and will forward your blurb to them when you are ready. A promise has a specific definition — and most things connectors say don't qualify.

If you leave a call unsure whether you have a promise, you don't. Log it as "hedged," send one follow-up, and if nothing comes back in a week, move on.

Tier 2 connectors — founders currently backed by your target funds — are your primary pipeline. Most of your intros will come from here. How you approach them matters.

- Get a warm intro to the founder first — Just like with investors, intros earn you credibility that make the ask easy.

- Send materials before the call — Share your deck or one-pager so they can see the company before you talk. Don't make them learn about you on the call itself.

- Ask for fundraising advice, not an intro — Opens the conversation naturally. "I'd love your perspective on our approach" is easier to say yes to than "can you intro me to your investors."

- Lead with your strengths — Don't bury the lede. Make it easy for them to see why this is worth forwarding.

- Bring them value — A useful connection, a sharp insight, genuine feedback on their product. Make the call worth their time.

- De-escalate the ask — "Would you be willing to forward a short blurb to [specific partner] to see if they'd be open to a meeting?" Not: "Can you intro me?"

- Always ask for more connectors at the end — "Who else do you know — investors or founders who've raised from funds in our space?" One conversation can multiply your network by 10–15×.

This applies to every connector call — Tier 0 through Tier 2. The goal of the call is one thing: walk away with a specific commitment to forward your blurb to a specific named partner.

After the call: Log immediately — promised or not. Note what they said, which investor they committed to, and the date. If they hedged, send one follow-up, then treat it as a no and move on. Don't let soft maybes inflate your pipeline.

- 60+ genuine promised intros from Tier 0–2 only

- Tier 3 intros logged separately — they're bonus, not core

- Every entry has a specific connector + specific investor + confirmed commitment

- Asked for more connectors at the end of every call

- Forwardable blurb drafted (Chapter 4 covers this — come back before you activate)

Prepare Your Pitch & Materials

By the time you get to your first investor meeting, your materials should be done — not drafted. Five materials. Different jobs. Different moments.

Before you write anything, lock your narrative. Every material flows from it. Three pillars:

Write in third person so your connector can forward it without rewriting a word. Always draft it yourself — it's your first impression, and it arrives before you do.

Test it with trusted advisors before it goes anywhere near an investor. Then AI stress-test: ask the model to respond as a skeptical investor and see what questions or objections surface.

Example blurb in context:

Standard 10-slide structure — a baseline. Decks are company-specific and iterative by nature.

Design: simple and readable, not flashy. Exception: consumer brands should invest in design. Lead with traction. Run a narrative test — can someone who's never heard of you follow the arc? Do AI objection prep before your first meeting.

A one-pager is a teaser, not a pitch deck. Its only job is to get a meeting. It should not answer every investor question or enable an investment decision on its own — think of it as a hook. Interesting enough to earn attention, not so comprehensive that a "no" can be made without a conversation.

The 7 Sections — in this order

Lead with your strongest asset. If you have traction, lead with that. If you're pre-revenue, lead with team.

What to leave out

Common mistakes that kill response rates

- Tiny font. If you're below 10pt, you're cramming. White space is not waste — walls of text discourage reading.

- Generic language. "Large market opportunity" is meaningless. "$12B market growing 15% annually" is not. Specific always beats vague.

- Wrong ordering. Lead with strength. Burying your best asset under sections you felt were expected is a common and costly mistake.

- Missing the ask. Every one-pager needs a clear, specific ask. Omitting it signals you don't have a process.

- Typos. Carelessness in writing signals carelessness in execution.

Example — finished one-pager

Here's a polished example for a fictional healthcare SaaS company — every section from the guide in practice. Notice:

- Header traction pills pull double duty — they confirm the company is real before an investor reads a word, and they create FOMO.

- Two-column split isn't arbitrary — Problem, Solution, and Market on the left tell the story. Team, Traction, and The Ask on the right are the proof.

- The Ask box is specific: amount, instrument, cap, committed capital, and use-of-funds tied to a milestone. That last line ("$300K MRR") signals Series A readiness.

- Deliberately left out: no exit section, no round name ("seed" vs. "pre-seed"), no financial projections. Those belong in the data room.

Build the structure now. Share only in Chapter 8, when you're in active diligence. Your job in the data room is to substantiate — not persuade.

Seven sections: Company overview, Financials, Cap table, Legal, Key contracts, Team, Metrics.

Cross-check everything for consistency with what you've said in meetings — inconsistencies, even small ones, kill deals that looked close. Use Docsend to track who views what and for how long — engagement signals are data. Gate behind a request: investors who ask are signaling serious intent.

Use AI for: narrative testing, objection preparation, competitive positioning benchmarking, blurb iteration, and transcript analysis after practice pitches. These are legitimate, high-leverage uses. Using it to write emails to investors is not.

Refine Through Practice

Your materials are ready, your intro pipeline is loaded. Before you pull the trigger, get comfortable enough with your pitch that you can focus on the conversation — not the content. You'll learn more from live investor meetings than from any practice session, which is exactly why you need a few reps before the ones that matter.

You get one first meeting per investor. Practice frees you to read the room instead of remembering what slide comes next. The goal isn't memorization — it's comfort. VCs invest in humans. Presence and energy can't be replaced by memorization, and they can't be learned in front of a mirror.

First meetings are typically 30 minutes: ~5 min intros, optional 5-min quick pitch, ~20 min Q&A. The deck sets the content trajectory — good founders drive the meeting on their terms.

How meetings evolve: the first meeting is lighter; subsequent meetings go deeper on specific areas; any time a new person enters the room, re-pitch from scratch.

Your pitch doesn't need to be perfect before you start. It needs to be good enough that you're comfortable — so your energy goes into the conversation, not the content. A few solid sessions with honest, experienced feedback is enough to get there. You will iterate through practice, but the most valuable iteration happens during live investor meetings. This is why you schedule throwaway pitches first — lower-priority investors early in your window to get your reps in before the meetings that matter.

Who to practice with (in order): Founders who recently closed > advisors with VC backgrounds > peers (early reps only) > AI (objection prep, not a substitute for human practice).

What to focus on: articulation, pacing, objection handling, energy. Record yourself and watch it back.

Develop your own filter for feedback. Weight by relevance — someone who has raised multiple venture rounds at your stage sees your pitch the way an investor will. Someone who hasn't raised before can still give useful signal, but focus specifically on clarity: "Is what I'm saying landing the way I intend it to?" rather than "Is this a compelling investment?" The weaker someone's fundraising context, the narrower the slice of their feedback you should act on.

- Narrative testing — Compare problem-led vs traction-led vs solution-led framings to find which lands best

- Objection simulation — Feed the deck and ask for investor-lens objections. Refine the slide that triggers the objection, not just the answer you give live

- Competitive positioning — Test whether your differentiation holds up to adversarial questioning

- Transcript analysis — Record every practice session, feed transcripts to AI with a consistent review prompt: "What came up? What landed? What did I deflect? What follow-up questions should I prepare for?"

Don't activate your intro pipeline until:

- You know your numbers cold — no hesitation on KPIs, unit economics, or model assumptions

- You can deliver the pitch conversationally without notes

- Top objections are identified and rehearsed

- Deck has been updated to address anything that consistently trips you up in practice

- Throwaway pitches are scheduled at the front of your window

Activate Your Intros

You have 60–100+ promised introductions loaded, your materials are ready, your pitch is sharp. The gun is loaded. Now you pull the trigger — all at once.

Trickling intros out over weeks creates a drip — not a signal. No urgency, no leverage, and your pitch evolves mid-process so early investors can't see the version later ones are seeing.

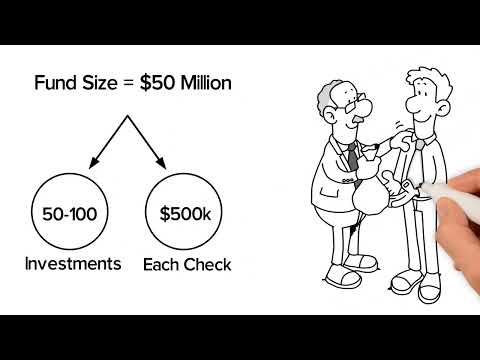

Example: $1.5M raise at $100K avg. check. Adjust for your round size.

This is why the 60–100+ promised intros from Chapter 3 exist. The buffer is intentional — not every promised intro converts to a meeting, and not every meeting converts to diligence.

The investor told your connector they wanted a meeting, the intro was made — and then nothing. This is not necessarily a hard pass; investors are busy and inbounds stack up.

Send one direct, brief follow-up: "Hi [name] — [connector] mentioned you were open to connecting. I'd love to find 30 minutes whenever works. Here's my calendar link: [link]." Make it as frictionless as possible.

If still no response after another week, log as "Paused" and stop following up. Re-engage when you have a term sheet — the dynamic completely changes.

Manage Your Pipeline

What gets measured gets managed. A fundraise without a CRM is a fundraise you're running from memory — and memory fails at exactly the wrong moments.

When you have 40–80 active investor conversations simultaneously, memory fails. The CRM isn't admin work — it's how you stay in control of a process that moves fast and in multiple directions at once. Without it, you follow up out of sequence, miss timing signals, and lose leverage you didn't know you had.

- Investor name + fund

- Tier (T1 / T2 / T3)

- Lead or follow

- Expected check size

- Stage

- Last activity date

- Next step — specific action + owner + timeline (never leave a meeting without this)

- Notes — objections raised, partner dynamics, specific interests flagged

Delays are data. Learn to read them:

- 2+ weeks to respond to intro request = low interest

- Difficulty scheduling first meeting = not actively moving

- Long gap between first and partner meeting = not championing internally

- Diligence goes quiet = likely de-prioritized

- Quick scheduling and fast replies = strong signal — prioritize and move fast

Log within 30 minutes of every meeting:

- Key objections — verbatim, not paraphrased

- What generated positive reactions

- Questions asked by the investor

- Partner dynamics mentioned

- Confirmed next steps with owner and timeline

Never leave a meeting without a confirmed next step. If the investor won't commit to one, that's a signal worth noting.

Run a standard AI review prompt on every transcript — record every session with a notetaker, feed transcripts to AI: "What came up? What landed? What did I deflect? What follow-up questions should I prepare for?" Track objection frequency across sessions. Pattern objections get fixed in the deck, not just handled live.

Diligence & Term Sheet

By the time an investor is in diligence, they're already interested. Your job is no longer to convince them — it's to confirm that everything you've said checks out. Clean, consistent, well-organized materials signal that you run a tight ship. Messy or inconsistent ones create doubt that's hard to walk back.

Watch for these signals and move fast when you see them:

- Reference calls requested

- Data room access requested

- Partner meeting scheduled

- Specific follow-up questions about metrics, unit economics, cap table, or model

You built the structure in Chapter 4. Now fully populate it. Seven sections:

Cross-check everything for consistency with what you've said in meetings. Inconsistencies, even small ones, kill deals that looked close. Use Docsend to track who views what and for how long — engagement signals are data.

Read the room. A strong first meeting with a fast-moving investor is a good candidate for proactive sharing. A lukewarm or exploratory conversation probably isn't.

This isn't about negotiating tactics yet — that's Chapter 9. This is vocabulary. Know it cold before you need it.

Valuation is a negotiation problem, not just a metrics question.

Close the Round

You have a lead investor, a term sheet, and a round to fill. Closing is its own phase — and founders consistently underestimate how much work it takes to get from "yes" to "wired."

You cannot fill a round without a lead. The lead sets the terms, leads diligence, and signals credibility to every follow-on investor. Getting to the first yes is the hardest part.

Once you have a lead, the dynamic of every follow-on conversation changes completely. Your Tier 1 list should have been built around lead investors first. Follow-on investors can be engaged earlier — they often want in before the lead is locked so they're not crowded out later.

With a signed term sheet, you're managing allocation — not selling the deal. The dynamics shift entirely.

- Re-engage Tier 2 and Tier 3 pipeline — investors who passed or went quiet often reverse on a credible term sheet

- Activate angels and small funds — they move faster and are less sensitive to valuation

- Set a clear allocation framework — know how much room you have and who gets priority

- Create urgency that's real — "We're closing the round in X weeks" is more effective when it's true

Not every raise closes the way it was planned. The honest version of this chapter includes what to do when the process stalls.

- Seed extensions are sometimes the right move. If you're close to Series A milestones but not quite there, a bridge or seed extension keeps the company alive. The CEO's primary job is to keep the company alive — do what the situation requires.

- Venture debt is an option with conditions. Requires proven unit economics, an established revenue model, and ARR minimums from debt partners. Not available to everyone, but worth evaluating.

- If investors are passing on the same issue, fix the issue. A pattern of the same objection across 15+ investor conversations is not bad luck — it's a signal. Address the root cause, then re-engage with updated data.

- A partial close is not failure. A smaller initial close with a plan to raise the remainder is often better than burning 6 months waiting for the perfect round composition.

- Go back and build — the process starts from Chapter 1

- You'll return with more data, more relationships, a stronger company

- A partial close or bridge is not failure — keeping the company alive is the job